Why Rhode Island Buyers Are Counting Themselves Out Before the Conversation Even Starts

I think about this more than almost anything else in my work.

The number of people in Rhode Island who have decided they cannot buy a home, without ever sitting down with a lender, without ever asking a single professional question, without ever actually knowing the real answer, is something that genuinely keeps me up at night.

Not because the market is easy right now. It is not. But because so many people are making a permanent decision based on incomplete information. And they are doing it alone, at 11pm, on their phone, with a Zillow estimate and a conversation they had with their coworker three months ago.

That is not a plan. That is a guess. And it is costing people more than they realize.

THE ASSUMPTIONS I SEE MOST OFTEN

"I cannot afford it."

This is the most common one. And it is almost always based on a number someone calculated in their head using a mortgage payment calculator and a home price they saw on Zillow. The problem is that calculation does not account for the programs available to them, the assistance they may qualify for, or what a lender would actually offer based on their full financial picture.

Rhode Island has down payment assistance programs available right now that most buyers have never heard of. There are loan options that require as little as 3% down. Some even less. The number you came up with at 11pm is almost certainly not the number a lender would give you.

"My credit is not good enough."

This one stops more buyers than almost any other assumption. And while credit absolutely matters in the home buying process, the threshold most people assume they need to hit is significantly higher than reality. There are lenders who work with credit scores that would genuinely surprise you. The only way to know where you stand is to have the actual conversation.

"I need 20% down."

This myth has been around for decades and it is still eliminating buyers who do not need to be eliminated. The 20% down rule is not a requirement. It is one option that helps you avoid private mortgage insurance. But it is far from the only path to homeownership. Most of the buyers I work with in Rhode Island put down significantly less than 20% and still closed on a home they love.

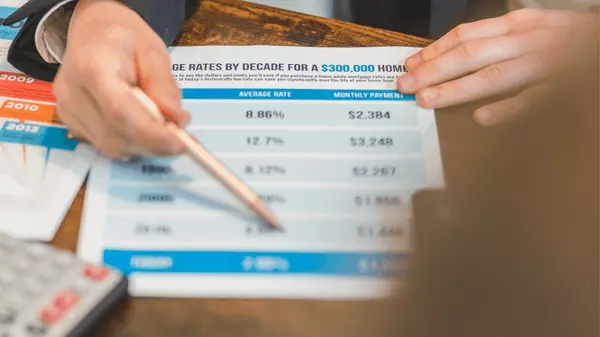

"Rates are too high right now."

Rates are higher than they were a few years ago. That is true. But the conversation around rates is almost always more nuanced than the headlines make it sound.

Here is how I approach this with every buyer I work with. Instead of starting with the rate, we start with the monthly payment. What number would you feel completely comfortable seeing leave your account every month? Not stretched. Not stressful. Comfortable. We build the search around that number first and let the rate be what it is.

When you shop by monthly payment instead of by rate, the rate loses its power over the decision. You are not chasing a number you cannot control. You are staying inside a budget that actually works for your life. And if rates drop in the future, you refinance and your payment gets better. That is a win that comes later. The home you are living in is the win that starts now.

Waiting for rates to drop means waiting alongside every other buyer who had the same idea. When rates fall, demand spikes, inventory tightens, and the competition you avoided by waiting shows up all at once. The market does not pause while you wait for perfect conditions. It keeps moving with or without you.

The buyers I have watched win in this market are not the ones who timed it perfectly. They are the ones who got honest about what they could comfortably afford, found a home that fit that number, and moved when there was still room to move.

THE REAL PROBLEM

The issue is not that people are asking questions. The issue is where they are getting the answers.

Your friend who bought a home in 2019 does not know what programs exist in 2026. Your family member who told you to wait does not know your specific financial situation. The Reddit thread you found at midnight does not know the Rhode Island market.

The only person who can tell you whether you can buy a home right now is a lender who has looked at your actual numbers. And the only way to get that answer is to ask.

I have watched people assume they were years away from buying and then sit down with a lender and find out they could have been in a home six months ago. I have watched people wait for the perfect moment and watch the market move past them. And I have watched people have one honest conversation and completely change the trajectory of what they thought was possible.

WHAT I WANT YOU TO DO

If you have been sitting with the question of whether homeownership is possible for you in Rhode Island, I want you to do one thing. Have the real conversation.

Not with your neighbor. Not with Google. With a lender who knows what is available right now and an advisor who knows this market specifically.

You might be closer than you think. And the only way to find out is to ask.

If you are ready to start that conversation reach out to me directly. I work with buyers across Rhode Island and Massachusetts and I am happy to point you toward the right resources, answer your questions honestly, and help you figure out what is actually possible for your situation right now. No pressure. No pitch. Just a real conversation.

Ready to find out where you actually stand? Connect with me here.

Categories

Recent Posts

GET MORE INFORMATION